[Models of Waqf]

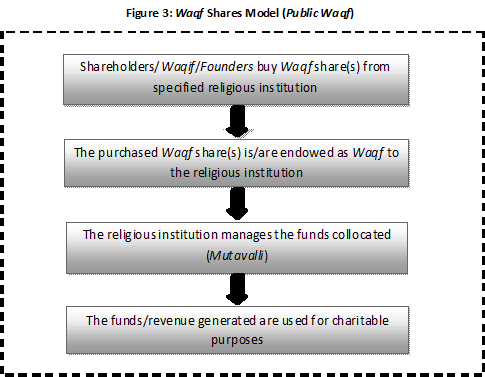

I) Waqf Shares Model:

This model is aPublic Waqf

which has been practiced in Malaysia, Indonesia, Sudan,

Kuwait and UK.

The procedure of this plan, in detail, is as follows (Magda Ismail Abdel Mohsin, 2008, P.9):

Founders

will buyWaqf

shares from specified religious institution with prices ranging between $1to $100 according to each country.

Founders

will receiveCash-Waqf

certificates as evidence that they purchaseWaqf

shares

with a specific amount.

TheseWaqf

shares will then be endowed to the issuing institution that will act as aMutawalli

to manage the collected fund.

The collected fund will then be distributed to charitable purposes as specified by the institution itself e.g. building mosques, schools, training center, etc.

This model can be clearly seen in following figure:

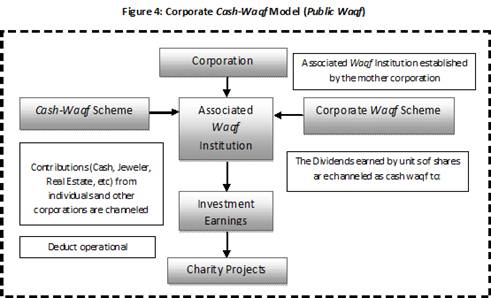

II) Corporate Cash-Waqf Model:

This model is a publicWaqf

which has been practiced in Malaysia specifically in KumpulanWaqf

an-Nur 1998, Turkey in Sabanci Foundation 1974, Pakistan in Hamdard Foundation 1953 and South Africa in the NationalAwaqaf

Foundation 2000. The Founder

in this model might be either an individual or a corporation.

The procedure of this plan, in detail, is as follows (Magda Ismail Abdel Mohsin, 2008, P.14):

Dividends earned for example by individuals, corporations will convey to an AssociatedWaqf

Institution asCash-Waqf

.

The AssociatedWaqf

Institution will act as aMutawalli

where manages and invests the accumulatedCash-Waqf

.

The revenue earned will then be directed to charitable projects after operational expenses have been deducted.

This model can be clearly seen in following figure:

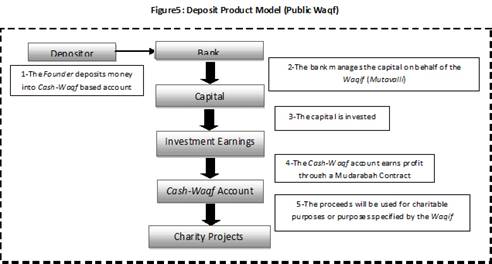

III) Deposit Product Model:

This model is aPublic

Waqf

which has been practiced in Bangladesh in two banks, the Social Investment Bank Limited (SIBL) and the Islamic Bank Bangladesh Limited)

IBBL).

The procedure of this plan, in detail, is as follows (Magda Ismail Abdel Mohsin, 2008, P.14 & 15):

Thefounder

deposits money intoCash-Waqf

based account in the bank.

While depositing the money, thefounder

will be given a list of theBeneficiaries

whereby he can chose or specify his/herBeneficiaries

.

The bank will act as aMutawalli

and will invest the capital throughMudzarabah Contract

.

The revenue generated will be channeled to charitable purposes or purposes specified by the founder.

This model can be clearly seen in following figure:

It has been realized as a good model whereMudzarabah

mode has been practice and at the same time theFounder

has the right to choose his/her ownBeneficiaries

.

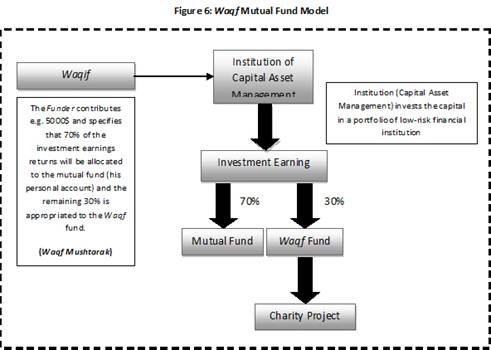

IV) Waqf Mutual Fund Model:

This model is a combinedWaqf

which has been practiced in Indonesia in the Dompet Dhuafa Batasa. This mutual fund is managed by the Batasa Capital Asset Management.

The procedure of this plan, in detail, is as follows (Magda Ismail Abdel Mohsin, 2008, P.16 & 17):

TheFounder

will contribute to the mutual fund, and at the same time he/she can contribute to theWaqf

fund. In this case theFounder

will specify for example 70% of his investment earnings return to the mutual fund i.e. his personal account and the remaining 30% will be appropriated to theWaqf

fund.

TheWaqf

institution will act as theMutawalli

to manage and invest the capital.

The investment earnings will then be distributed according to theFounder

condition where 70% will go for his mutual fund and 30% will go toWaqf

fund and distributed to charity projects, as highlighted below.

This model can be clearly seen in following figure:

From the above model it may be seen that it isWaqf Mushtarak

, but in this case the capital of the 70% and the revenue generated from investing this portion will go back entirely to theFounder

leaving the 30% asCash-Waqf

.

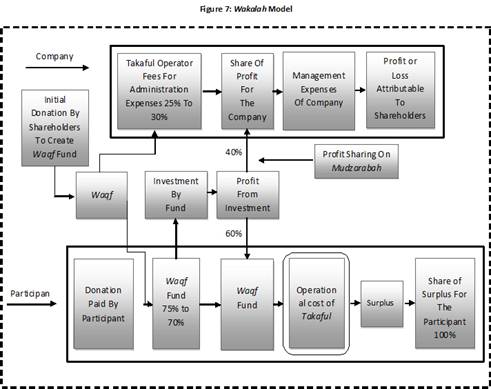

V) Wakalah with Waqf Fund:

This model is aPublic

Waqf

which has been practiced in Pakistan and Malaysia.

The procedure of this plan, in detail, is as follows (Abdul Rahim Abdul Wahab, 2006, P.11)

The Shareholders would initially make a donation to establish theWaqf

fund. The donation can be of any reasonable amount (Shariah scholars may specify such an amount). After the creation of theWaqf

fund the Shareholders would lose their ownership rights on theWaqf

fund and would become the property of theWaqf

fund. However, they will have the right to administer and develop rules and regulations of the fund.

The original donation of theWaqf

fund needs to be invested in a very safeShariah

compliant investment and its returns would be used for the benefit of the participants. The idea being that theWaqf

fund should remain intact with high likelihood.

Company would take this donation on behalf of theWaqf

fund as administrator of the fund and deposit this in the fund.

The donations received from the participants, seekingTakaful

protection, would also be a part of this fund and the combined amount will be used for investment and the profits earned would again be deposited into the same fund. As perWaqf

principles, a member (donor) can also benefit from theWaqf

fund.

This model can be clearly seen in following figure:

Establishment of a Cash-Waqf Financial Institution (CWFI):

Inasmuch as the above models are just associated with some instrument to simplify poverty alleviation, one or several persons can not implement them in real. So we require to some institutions or corporations that have high capability, skill and enough experiences to implementing our goal (Poverty alleviating viaCash-Waqf

models).Cash-Waqf

management institution should manage the accumulatedCash-Waqf

created by the differentFounders

in such a way that the collected fund becomes more and more productive. The more theWaqf

investment return, the moreMawquf

‘alaih

benefit fromWaqf

fund. Only gains of the investedWaqf

fund will be delivered toMauquf

'alaih

and the principal of fund keep being invested in potential investment opportunities.

Islamic (Shia) school's approach on these models:

With reference to all models that are presented, we consider the Islamic approach about them in order to state which of them is acceptable.

Although, in regards with Islam School's approach, "Waqf

Shares Model, CorporateCash

-Waqf

Model,Waqf

Mutual Fund Model and Cooperative Model" are admissible, butWakalah

Model is not admissible. In follow we will concern to each model for stating more points about them.

Waqf

Shares Model,Waqf

Mutual Fund Model & Cooperative Model:

However, for these models, two important things are not clearly highlighted for the creation ofCash

-Waqf

:

TheFounder

of theWaqf

has no choice in specifying his/herBeneficiaries

as this might discourage moreFounder

to createCash-Waqf

.

It is very difficult to ensure the element of perpetuity of theCash-Waqf

as it is not clear how theCash-Waqf

is invested and how to ensure the capital is intact.

Corporate Cash-Waqf Model:

According to this model, AssociatedWaqf

Institution that established by the mother corporation, channel accumulated Cash to investment after deducting operational expenses. IfWaqif

mentions this condition inWaqf Contract

, it will be valid. Otherwise it will be void and AssociatedWaqf

Institution won’t be allowable to deduct operational expenses from earned revenues.

Deposit Product Model:

In this model we should consider that theFounder

mustn't be allowable to withdrawal his contributions from deposit account after some times. Because one of most important conditions onWaqf Contract

is "TheMawquf

(i.e. cash) should be perpetual". This model will be admissible, ifFounders

follow this way.

Wakalah Model:

One of most important conditions onWaqf Contract

is "TheFounder

mustn't allocate any part of revenue fromCash

-Waqf

toward himself ". But in this model, as appeared, this condition isn’t followed. So, according to Islam jurisprudence, it will be void

0%

0%

Author: Majid Khademolhoseini

Author: Majid Khademolhoseini